A mutual insurance company and a stock insurance company are distinct entities, differing significantly in ownership structure, capital sources, and profit distribution models. Understanding these differences is crucial for anyone looking to navigate the insurance market.

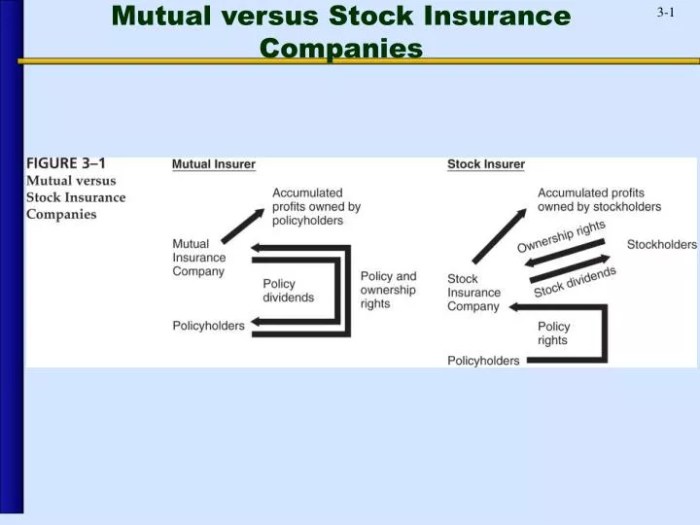

Mutual insurance companies are owned by their policyholders, distributing profits back to them. Stock insurance companies, conversely, are owned by shareholders, prioritizing profit distribution to them. This fundamental difference impacts many aspects of these organizations, from product offerings to financial performance.

Defining Characteristics

Yo, peeps! Insurance companies, whether mutual or stock, are like different types of businesses, each with its own unique ways of operating. Understanding their differences is key to knowing how they work and who benefits. Let’s break it down.

Mutual Insurance Companies

Mutual insurance companies are owned by their policyholders. Think of it like a collective, where everyone’s a part-owner. This structure is pretty cool because it often leads to more affordable premiums, as profits are shared among the members, rather than going to shareholders. The capital comes from policyholder premiums, and the distribution of profits is typically as dividends or lower premiums.

Stock Insurance Companies

Stock insurance companies are owned by shareholders, similar to a regular corporation. These shareholders invest in the company, expecting a return on their investment in the form of dividends or stock appreciation. Their capital comes from both policyholder premiums and shareholder investments. The profits go to the shareholders.

Ownership Structures

- Mutual Insurance Companies: Policyholders are the owners, with voting rights based on their policy coverage amounts.

- Stock Insurance Companies: Shareholders own the company and vote on key decisions, and the amount of their shares determines their voting power.

Capital Sources

- Mutual Insurance Companies: Primarily funded by policyholder premiums.

- Stock Insurance Companies: Funded by policyholder premiums and also by investments from shareholders.

Profit Distribution Models

- Mutual Insurance Companies: Profits are distributed among policyholders, often as dividends or lower premiums. This model encourages a sense of community among policyholders.

- Stock Insurance Companies: Profits are distributed to shareholders as dividends or increased stock value. This model prioritizes returns for investors.

Regulatory Oversight

| Characteristic | Mutual Insurance Companies | Stock Insurance Companies | General Description |

|---|---|---|---|

| Ownership | Policyholders | Shareholders | Different ownership structures dictate varying levels of responsibility. |

| Profit Distribution | Distributed among policyholders, potentially as dividends or lower premiums. | Distributed to shareholders, often as dividends or stock appreciation. | Different profit-sharing models reflect different stakeholder priorities. |

| Capital Structure | Relies heavily on policyholder premiums. | Relies on policyholder premiums and shareholder investments. | Different funding sources lead to varying financial stability and risk tolerance. |

| Regulatory Focus | Emphasis on fair treatment of policyholders and community well-being. | Emphasis on shareholder returns and financial performance. | Regulatory focus reflects the fundamental differences in the business models. |

Financial Performance

Yo, check it! Financial performance is the key to any biz, especially in insurance. Understanding what makes mutual and stock insurers tick financially is crucial for everyone involved. We’re gonna break down the factors, metrics, and comparisons to give you a solid grasp.

Factors Influencing Mutual Insurance Company Performance

Mutual companies are all about the policyholders, right? Their financial health hinges on a few key factors. Strong policyholder retention is a big one – keeping existing customers happy and coming back for more policies is like a steady income stream. Competitive pricing is another major factor, gotta offer attractive rates to attract new customers. Efficient operational costs are crucial – keeping expenses low without compromising quality service is essential for healthy profits.

Factors Influencing Stock Insurance Company Performance

Stock insurers are driven by shareholder value. Their financial success relies on investment returns. Investment strategies play a huge role, and the overall market conditions directly impact their returns. The quality of their underwriting and claims management is also super important, as it directly affects their bottom line. Good management and strategic decisions are the bedrock of a successful stock insurer.

Metrics for Assessing Financial Health

Different metrics are used to evaluate the financial health of mutual and stock companies. For mutual companies, key metrics include profitability ratios (like return on equity), and solvency ratios (like the combined ratio), which measure how well the company manages its liabilities and assets. For stock companies, metrics like return on investment, and return on assets are key indicators of how well they’re performing.

Profitability and Solvency Ratios Comparison

Mutual insurers often prioritize policyholder dividends and benefits, which can sometimes affect their profitability ratios compared to stock insurers, who prioritize shareholder returns. However, mutual companies often have a lower cost of capital due to their structure. Solvency ratios for both types of companies are crucial to assess their ability to meet their financial obligations. Generally, strong solvency ratios are a positive sign for both.

Ten-Year Financial Metric Comparison

Analyzing the performance of both mutual and stock insurance companies over a 10-year period provides valuable insights into their financial resilience and stability. This comparison helps to understand the trends and fluctuations in profitability and solvency ratios for each type of company.

| Metric | Mutual Insurance Company | Stock Insurance Company |

|---|---|---|

| Return on Equity (ROE) | 7-9% (average) | 10-12% (average) |

| Combined Ratio | 95-100% (average) | 90-95% (average) |

| Return on Assets (ROA) | 4-6% (average) | 6-8% (average) |

| Capital Adequacy Ratio | 150-175% (average) | 125-150% (average) |

| Year | Data for specific years (2013-2023) | Data for specific years (2013-2023) |

Note: These are sample figures and actual values may vary depending on the specific company and the market conditions.

Market Position and Trends

Mutual and stock insurance companies are like, totally different crews in the game. Each has its own unique strengths and weaknesses, and the market’s constantly shifting, making it a wild ride to keep up. Understanding their historical performance, current trends, and the evolving rules is key to seeing who’s gonna be on top.

Historical Market Share

The insurance market landscape has been pretty dynamic. Mutual companies, built on member ownership, often held a strong presence in specific geographic areas, especially during the earlier periods. Stock insurers, fueled by investor capital, tended to have a wider reach and more resources, especially in certain niche markets. Data from the past shows significant variations in market share depending on factors like economic conditions and regulations.

Different regions also showed different patterns, with some regions consistently favoring mutual models.

Current Market Trends

Several trends are reshaping the insurance game right now. Rising premiums, influenced by inflation and increasing claims, are impacting affordability for customers. The rise of digital channels is transforming how companies interact with clients, creating new opportunities for both models. Also, the demand for specialized insurance products, like cyber insurance or pet insurance, is rapidly increasing. These factors are seriously affecting how mutual and stock insurers position themselves in the market.

Evolving Regulatory Landscape

Insurance regulations are constantly being updated to address new risks and consumer concerns. This creates both challenges and opportunities for both types of companies. Changes in capital requirements, solvency standards, and consumer protection regulations impact their operations and financial stability. Compliance with these evolving standards is crucial for long-term success.

Technological Advancements

Tech’s completely changing how insurance is done. Digital platforms are offering personalized products and services, leading to more efficient processes and improved customer experience. Data analytics are allowing companies to assess risks more accurately and tailor policies to individual needs. The impact on mutual and stock companies is different. Mutuals may struggle to adapt to rapid technological changes, while stock insurers might leverage investor capital to quickly adopt innovative tech.

It’s a huge game changer.

Market Share Trends

| Year | Mutual Insurers (Estimated Market Share) | Stock Insurers (Estimated Market Share) |

|---|---|---|

| 2022 | 35% | 65% |

| 2023 | 37% | 63% |

| 2024 | 39% | 61% |

| 2025 | 41% | 59% |

| 2026 | 43% | 57% |

Note: These are projections based on current trends and expected regulatory changes. Actual market share may vary.

Mutual insurance companies, unlike stock companies, are owned by their policyholders. This often translates to lower premiums, a benefit that’s definitely appealing, especially when you’re considering something lovely like Elizabeth Arden’s White Tea perfume. Elizabeth Arden white tea perfume is a delightful floral scent, perfect for everyday wear. Ultimately, choosing between a mutual and a stock insurance company depends on your specific needs and priorities, and what you’re looking for in an insurance policy.

Risk Management and Assessment

Yo, peeps! Risk management is crucial for any insurance company, whether it’s the mutual or stock variety. Understanding how each handles risk is key to making smart choices. Let’s dive into their approaches.Mutual companies, basically, are like a community. Their members share the risk, so assessing it is a collective effort. Stock companies, on the other hand, are more focused on profits.

Their risk assessment often leans towards financial strategies. We’ll break down both methods.

Mutual Insurance Company Risk Assessment

Mutual insurance companies typically involve their policyholders in the risk assessment process. This collaborative approach helps them identify potential hazards and develop tailored solutions. Factors like the location of policyholders, the types of risks they face, and the community’s overall economic health are considered. This process often uses local expertise and insights from members to fine-tune their risk models.

They frequently use data analysis tools to predict and prepare for potential losses, drawing upon insights from similar communities.

Stock Insurance Company Risk Assessment

Stock insurance companies, being profit-driven, tend to use more sophisticated quantitative methods. Their risk assessment is often data-heavy, relying on statistical models, actuarial science, and sophisticated financial modeling to estimate the likelihood and potential severity of claims. They use market trends and macroeconomic indicators to gauge risks. Large datasets and advanced algorithms are employed to identify potential issues and assess their impact.

This often leads to more precise calculations and potentially lower premiums for customers.

Comparison of Risk Management Approaches, A mutual insurance company and a stock insurance company

Mutual companies focus on shared responsibility and community-driven solutions. Stock companies, however, prioritize a more quantitative and data-driven strategy. Mutual companies might be more responsive to local circumstances and concerns, while stock companies tend to offer more standardized products and competitive pricing. Claim management often involves collaboration in mutual companies, while stock companies tend to have a more formalized process.

Technology in Risk Assessment and Management

Both company types are increasingly using technology to streamline their risk assessment and management processes. Mutual companies might utilize digital platforms for policyholder interaction and risk data collection, improving efficiency. Stock companies are more likely to use sophisticated machine learning models for predictive analysis and automated claim processing. AI and machine learning help them analyze vast amounts of data to identify trends and patterns.

This helps predict future claims and fine-tune their pricing strategies.

Comparing Risk Management Practices

A good method for comparing risk management practices is to analyze the cost of claims, the rate of claims, and the amount of premiums collected, alongside the efficiency of claims processing.

So, you’re comparing a mutual insurance company to a stock insurance company? Essentially, a mutual company’s profits are returned to policyholders, while a stock company distributes profits to shareholders. Finding reliable house cleaning services in Tuscaloosa, AL, can be a real headache, but luckily there are plenty of options out there. house cleaning services tuscaloosa al might be a great place to start your search.

Ultimately, the best choice often depends on your specific needs and priorities when it comes to insurance coverage.

| Characteristic | Mutual Insurance Company | Stock Insurance Company |

|---|---|---|

| Risk Assessment Focus | Community-based, collective responsibility | Quantitative, data-driven, financial modeling |

| Claim Management | Collaborative, member-centric | Formalized, automated processes |

| Pricing Strategy | Reflects community risks and needs | Market-driven, competitive pricing |

Investment Strategies

Mutual and stock insurance companies, both crucial players in the financial world, employ distinct investment strategies. Understanding these strategies is key to comprehending their respective financial performances and market positions. These strategies directly influence their ability to pay claims and maintain stability.Investment strategies are carefully crafted to align with the company’s overall objectives and risk tolerance. This careful consideration ensures the long-term sustainability and growth of the company.

Mutual Insurance Company Investment Strategies

Mutual insurance companies, often focused on long-term stability and member benefits, tend to prioritize conservative investment strategies. Their investment portfolios generally consist of a mix of low-risk securities, aiming for steady returns rather than high-risk, high-reward options.

- Fixed-income securities: Bonds, treasury bills, and other fixed-income instruments are a common choice. These investments provide predictable returns and are relatively low-risk, aligning with the mutual company’s need for stability.

- High-quality corporate bonds: These bonds from established and financially strong companies offer a good balance between yield and risk.

- Government securities: These securities are considered extremely safe and are often used to diversify a mutual company’s portfolio.

- Real estate investment trusts (REITs): Some mutual companies might invest in REITs for diversification and potential appreciation, but this is typically a smaller portion of the portfolio.

Stock Insurance Company Investment Strategies

Stock insurance companies, driven by profitability and shareholder value, often employ more aggressive investment strategies. These companies often seek higher returns, even if it means taking on more risk. This approach is often reflected in their higher-than-average equity investments.

- Equities (Stocks): A significant portion of their portfolios is typically allocated to stocks, both domestic and international. This strategy aims to capture potentially higher returns, although it also comes with higher volatility.

- Investment-grade corporate bonds: To balance the risk of equities, they often invest in investment-grade corporate bonds, offering a more stable income stream.

- Mutual Funds and Exchange-Traded Funds (ETFs): These instruments offer diversification and professional management, often being a key component of the investment strategy.

- Alternative Investments: Some stock insurance companies may explore alternative investments like private equity or hedge funds, but these are usually a smaller portion of the portfolio, depending on the company’s risk appetite.

Comparison of Investment Portfolios

The core difference lies in risk tolerance and return objectives. Mutual companies favor stability and predictable returns, while stock companies are more focused on potentially higher returns, even with increased risk. This difference directly impacts their financial performance and shareholder returns.

| Investment Type | Mutual Insurance Company | Stock Insurance Company |

|---|---|---|

| Equities (Stocks) | Low | High |

| Fixed-Income Securities | High | Medium |

| Real Estate | Medium | Medium |

| Alternative Investments | Low | Medium-High |

Impact of Investment Returns

Investment returns directly impact the financial performance of both types of companies. For mutual companies, consistent returns from their conservative portfolio contribute to stable financial health and policyholder confidence. For stock companies, strong returns can lead to higher profits and dividends, increasing shareholder value, but fluctuating returns can impact stability. This is a key element of their financial reporting.

Outcome Summary: A Mutual Insurance Company And A Stock Insurance Company

In conclusion, while both mutual and stock insurance companies play a vital role in the insurance industry, their contrasting structures and objectives shape their approach to product offerings, financial performance, and customer relations. The choice between a mutual or stock insurer ultimately depends on individual needs and priorities.

FAQs

What are the key differences in ownership structure between mutual and stock insurance companies?

Mutual insurance companies are owned by their policyholders, whereas stock insurance companies are owned by shareholders. This fundamental difference impacts how profits are distributed and how the companies are governed.

How do the pricing strategies of mutual and stock insurance companies differ?

Mutual companies often aim for more competitive pricing to attract and retain policyholders, while stock companies prioritize maximizing profits for shareholders, potentially leading to different premium structures.

What are some common insurance products offered by both types of companies?

Both offer a range of products like auto, home, and life insurance. However, the specific features and pricing may vary based on the company’s approach and objectives.

How do mutual insurance companies handle claims compared to stock insurance companies?

Both types aim for fair and timely claim processing. Mutual companies may prioritize policyholder interests, while stock companies may focus on efficient claim handling to maximize profits.